AP Microeconomics : Side-by-Side Graphs

Study concepts, example questions & explanations for AP Microeconomics

All AP Microeconomics Resources

Example Questions

Example Question #1 :Output

假设好Y的价格增加了5%。If the quantity supplied of Good Y remains constant, then the price elasticity of supply of Good Y is ________.

greater than 1.

less than 0.

impossible to determine from the information given.

0.

1.

0.

Remember that the price elasticity of supply is calculated by taking the percent change of the quantity supplied (in this case 0%) divided by the percent change in the price (in this case 5%). So the price elasticity of supply of Good Y is 0.

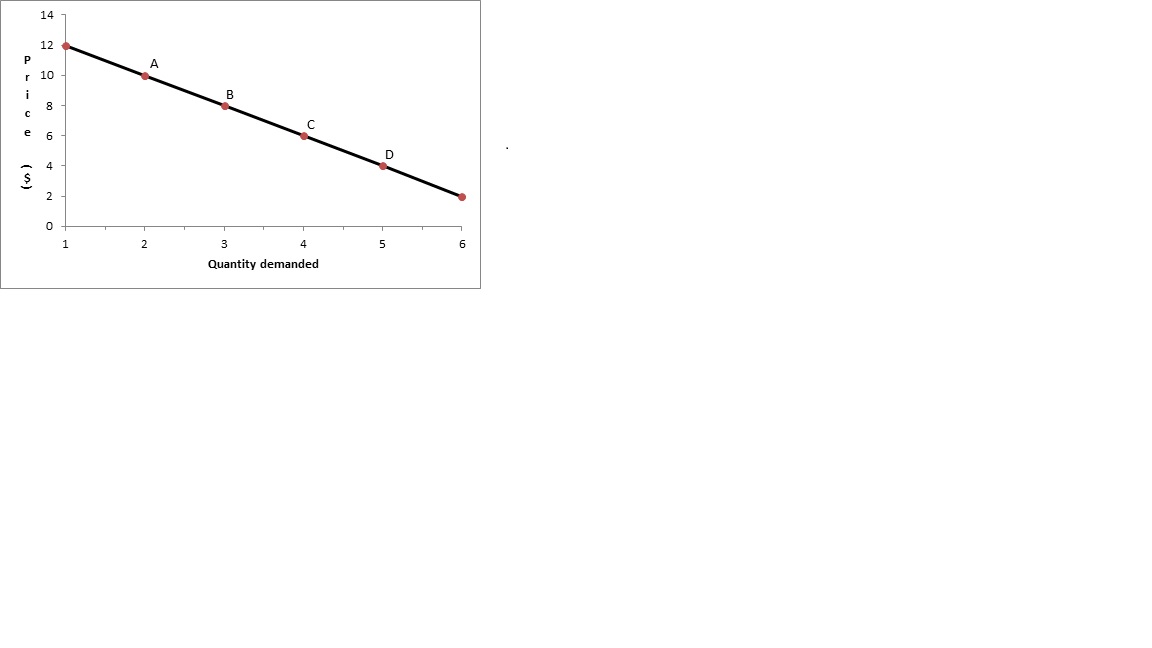

Example Question #11 :Microeconomics Graphs

Use the following graph for questions 9 - 11

Increasing the price of oranges at point D will result in:

- An increase in total revenue

- A decrease in quantity demanded

- Movement toward a portion of the demand curve that is more elastic

2 only

1, 2, and 3

3 only

1 only

1 and 2

1, 2, and 3

If we are in the inelastic portion of the demand curve, an increase in price will increase TR, since the price effect is greater than the quantity effect. Quantity will still decrease.

Example Question #2 :Short Run Earnings

Use the following graph to answer questions 9-11:

What is the total revenue generated at point A?

10

30

24

20

12

20

Total revenue is price multiplied by quantity (TR = P x Q). At point A, price is $10 and quantity is 2, so TR = 2 x 10 = 20.

Example Question #1 :Long Run Market Equilibrium

A price ceiling that is set above the market equilibrium price is likely to have which of the following effects, if any?

A surplus

No effect; price will never equal market equilibrium price

A shortage

No effect; price will equal market equilibrium price.

No effect; price will equal market equilibrium price.

If a price ceiling is set above market equilibrium, market forces will cause the equilibrium price to be market equilibrium price. The price ceiling will never be reached because it is too high.

创建一个有效的价格上限,hand, the price ceiling must be set below market equilibrium price, thus stopping price levels before they can reach market equilibrium. In such a case, a shortage is expected.

Example Question #2 :Long Run Market Equilibrium

If good X and good Y are substitutes, an increase in the price of good X will lead to which of the following?

a decrease in demand for good Y

an increase in demand for good Y

a decrease in supply for good Y

an increase in supply for good Y

an increase in demand for good Y

The change in price of a substitute good shifts demand.

An increase in the price of good X prompts consumers to use good Y instead of good X (i.e. substituting good X for good Y), resulting in increased demand for good Y.

Example Question #3 :Long Run Market Equilibrium

As consumption of a particular good increases, the satisfaction gained from consuming one additional unit of the good eventually ___________.

equals 0

increases

decreases

equals 1

decreases

The law of diminishing marginal utility states that as consumption of a particular good increases, the satisfaction gained from consuming one additional unit (i.e. the marginal utility of the good) eventually decreases.

For example, consider eating chocolate bars. The increase in satisfaction resulting from eating the first chocolate bar is probably higher than the increase in satisfaction from eating the 12th chocolate bar. In other words, the marginal utility has decreased.

Example Question #4 :Long Run Market Equilibrium

If the market for Good X is in equilibrium, which of the following would NOT cause a decrease in demand for Good X?

The price of a substitute good decreases.

Consumers expect that the price of Good X will decrease.

The number of buyers of Good X decreases.

The price of a substitute good increases.

A newspaper reports that Good X is harmful to the health of consumers.

The price of a substitute good increases.

Of the five answer choices, only an increase in the price of a substitute good would cause the demand curve to increase. This result reflects the fact that when the price of the substitute good increases, consumers are less likely to buy that good and instead buy more of Good X.

All of the other answer choices would cause the demand curve to decrease.

Example Question #11 :Microeconomics Graphs

For any firm, the long run refers to a period of time in which ________.

variable costs are able to change

fixed costs are able to change

sunk costs are able to change

the price elasticity of supply is able to change

fixed costs are able to change

The definition of the long run is a period of time in which fixed costs are able to change. For example, in the long run, a firm can move to a new plant that costs less money to operate each month.

Sunk costs are costs that cannot be recovered and therefore would not change, even in the long run.

The price elasticity of supply refers to the responsiveness of the supply curve to a change in price.

Example Question #12 :Microeconomics Graphs

实现利润最大化,企业生产水平which _________.

marginal revenue is less than marginal cost

marginal revenue equals average total cost

marginal revenue equals marginal cost

marginal revenue equals average variable cost

marginal revenue equals marginal cost

The profit maximizing rule for the firm is marginal revenue equals marginal cost. Notice that the rule does not explicitly involve average total or average variable costs.

The MR=MC profit maximizing rule holds for all market structures - monopoly, oligopoly, monopolistic competition, and perfect competition.

If marginal revenue is less than marginal cost, then the firm actually loses profits with continued production.

Certified Tutor

Certified Tutor

All AP Microeconomics Resources